Earning well feels like the hard part. For most people who reach senior roles, build successful businesses, or finally break through into six-figure salaries, the assumption is that strong income translates directly into financial progress.

It often does not. Crossing certain income thresholds in the UK does not just mean paying more tax.it means losing allowances, forfeiting benefits, and quietly paying effective tax rates that most people would find shocking if they saw them written down. The challenge for high earners is rarely how much they make. It is how much they actually keep.

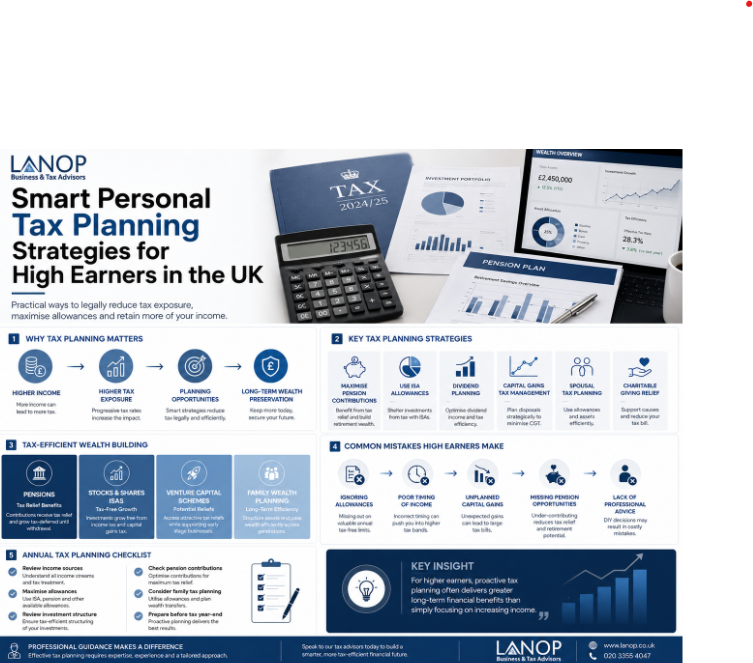

Personal tax planning is what changes that equation. Not through loopholes or aggressive schemes, but through a clear understanding of how the tax system works and making deliberate decisions before the bill arrives rather than after.

Why Do High Earners Often Feel Financially Stuck?

There is a particular frustration that hits somewhere around the £80,000 to £100,000 mark. The salary is strong. The lifestyle reflects it. But the gap between gross income and actual financial progress feels smaller than it should.

Part of that is lifestyle inflation spending tends to rise with income, almost automatically. But a significant part is tax drag. The more you earn, the more efficiently HMRC collects, and the less efficiently most people plan. A pay rise at this level often delivers far less in take-home pay than the gross figure suggests, and in some cases almost nothing at all.

The real goal is not maximising income. It is maximising what you actually retain, build, and eventually pass on.

The Hidden Tax Traps That Catch High Earners Off Guard

The £100,000 Threshold

This is the number that surprises people most. In the UK, the Personal Allowance the amount you can earn tax-free starts tapering once your adjusted net income exceeds £100,000. For every £2 you earn above that figure, you lose £1 of your Personal Allowance. By £125,140, the allowance is gone entirely.

The practical consequence is an effective 60% tax rate on income between £100,000 and £125,140. Income Tax at 40% plus the loss of the allowance creates a band where earning more genuinely costs you more in proportion than almost anywhere else in the tax system.

Consider this scenario. You earn £115,000 and receive a £10,000 bonus. That bonus does not just attract 40% tax. It pushes more of your income into the taper zone, accelerating the Personal Allowance withdrawal. The effective rate on that bonus could sit at 60% or above. You receive £10,000 gross and keep considerably less than half.

The Allowances and Benefits That Quietly Disappear

| Income Level | What You Start to Lose? |

| £50,000+ | High Income Child Benefit Charge begins 1% clawed back per £100 over |

| £60,000+ | Child Benefit fully withdrawn |

| £100,000+ | Personal Allowance taper begins effective 60% rate |

| £100,000+ | Free childcare hours (30 hours) lost for under-fives |

| £125,140+ | Personal Allowance gone entirely |

| £150,000+ (previously) | Additional rate now caught earlier under current thresholds |

Most professionals discover these losses during their first Self Assessment filing, not before. By then the income has already been received and the planning window has closed.

Smart Ways to Reduce Taxable Income Legally

Pension Contributions More Powerful Than Most Realise

Pensions are not just a retirement tool. For high earners, they are one of the most effective mechanisms for managing adjusted net income and recovering lost allowances.

Contributions attract tax relief at your marginal rate. For a 40% taxpayer, every £800 contributed costs £800 personally but £1,000 lands in the pension with basic rate relief added automatically and higher rate relief claimed through Self Assessment. For someone in the 60% effective band, the relief is even more valuable.

The mechanism that makes this particularly powerful is the reduction in adjusted net income. A person earning £115,000 who contributes £15,140 to their pension brings their adjusted net income back below £100,000. The Personal Allowance is fully restored. The effective saving on that contribution is not 40%,it is closer to 60% when the restored allowance is factored in.

The annual allowance currently sits at £60,000, though it tapers for very high earners above £260,000. For most people in the £100,000 to £200,000 range, significant headroom exists.

Salary Sacrifice

Salary sacrifice works by replacing part of your salary with a non-cash benefit pension contributions being the most common. The reduction in gross salary reduces both Income Tax and National Insurance. Employers also save on Employer NI, which means some firms pass part of that saving back to the employee.

The most common mistake is treating salary sacrifice as exclusively a pension strategy. It also applies to electric vehicles through company car schemes, cycle to work arrangements, and additional employer pension contributions. Each reduces the gross salary figure and the taxable income that flows from it.

Gift Aid

Charitable donations under Gift Aid allow the charity to reclaim basic rate tax, but the higher rate relief belongs to the donor. A £1,000 Gift Aid donation costs a 40% taxpayer £750 after relief. It also reduces adjusted net income which matters enormously to anyone sitting near the £100,000 or £50,000 thresholds.

The Figure That Controls Everything(Adjusted Net Income)

Most tax conversations focus on salary. The figure that actually determines your tax position is adjusted net income, your total income minus specific deductions including pension contributions, Gift Aid, and trading losses.

This single number determines whether your Personal Allowance survives, whether you pay the High Income Child Benefit Charge, whether your children qualify for free childcare hours, and how much higher rate relief you can claim. Almost every significant planning decision for a high earner ultimately connects back to it.

The practical implication is straightforward. If your adjusted net income sits at £105,000, you are losing £2,500 of your Personal Allowance. A pension contribution of £5,001 brings you back below £100,000 and restores it entirely. The net tax saving on that contribution is significantly higher than the headline relief rate suggests.

Tax Planning for Bonuses and Equity Compensation

Bonuses create timing problems. Received in the wrong month, they push you into a higher band or accelerate allowance withdrawal. Received with proper planning in place, the tax cost can be significantly reduced through pension contributions timed to coincide with the bonus payment.

Before accepting a large bonus, ask three questions. Where does my adjusted net income currently sit? Will this bonus push me across a meaningful threshold? And is there a pension contribution I should make this tax year to offset the impact?

Equity compensation RSUs, share options, and share awards is where planning is most frequently absent. Technology sector employees and finance professionals often receive substantial equity packages without any structured thinking about the tax consequences at vest, exercise, or sale.

RSUs are taxed as income at the point they vest. That vesting event can push adjusted net income significantly above normal salary levels, triggering all the threshold consequences described above. Planning around vesting dates, pension contributions, and capital gains on subsequent disposal can make a material difference to the final tax cost.

Investment Strategies That Improve Tax Efficiency

ISAs

The ISA allowance is £20,000 per year. Growth and income within an ISA attract no tax, no Capital Gains Tax on disposal, no Income Tax on dividends or interest. For high earners whose savings allowance is restricted and whose dividend allowance is reduced, ISAs are not just useful. They are essential.

The compounding effect over a decade of full ISA contributions is substantial. The tax-free status applies permanently, not just during the contribution phase.

Capital Gains Management

Capital Gains Tax applies to asset disposals above the annual exempt amount, which has been significantly reduced in recent years. The rate for higher rate taxpayers is 24% on residential property and 18% for other assets following recent changes.

The key planning principle is timing. Spreading disposals across tax years, transferring assets between spouses before disposal, and matching gains with losses already crystallised in the portfolio all reduce the effective CGT exposure.

VCTs and EIS

Venture Capital Trusts and Enterprise Investment Schemes offer Income Tax relief of 30% on qualifying investments, alongside CGT deferral and exemption benefits. They carry higher risk than mainstream investments and suit a specific profile, typically high earners with tax liabilities they want to offset and appetite for early-stage company exposure.

These are not suitable for everyone. But for the right investor, they represent legitimate and HMRC-approved ways to reduce a significant tax bill while gaining investment exposure.

The Area Most People Ignore(Family Tax Planning)

Household Strategy

Tax planning works most efficiently at household level rather than individual level. Two partners with asymmetric incomes have opportunities that a single high earner does not.

Transferring income-producing assets to a lower-earning spouse shifts the tax liability to a lower rate. Married Couple’s allowance transfers, pension contributions for non-working spouses, and joint ISA strategies all contribute to a more efficient household tax position.

Protecting Childcare Support

Here is a scenario that plays out frequently. Both parents work. Combined income is well above £100,000. But one parent earns £99,000 and the other earns £30,000. The higher earner is below the personal allowance taper threshold. Their children qualify for 30 hours of free childcare. The value of that benefit can exceed £5,000 per year.

Now that parent receives a pay rise to £102,000. Adjusted net income crosses £100,000. Free childcare disappears. The pay rise generated additional tax and cost the family thousands in childcare support.

A pension contribution of £2,001 restores the adjusted net income below £100,000. The free childcare is retained. The pension grows. The net financial outcome is significantly better than accepting the pay rise without any planning.

Seven Costly Mistakes High Earners Commonly Make

Focusing only on income. Gross salary is not the metric that matters. Adjusted net income is.

Ignoring key thresholds. £50,000, £60,000, £100,000, £125,140 each carries specific consequences that most professionals discover too late.

Missing pension opportunities. The annual allowance is generous for most high earners. Using it consistently compounds into genuinely life-changing sums.

Forgetting family planning. A household strategy almost always outperforms an individual one.

Holding investments inefficiently. Assets generating income outside ISAs and pensions attract tax unnecessarily. Structure matters as much as selection.

Failing to review annually. Income changes. Thresholds change. Planning done three years ago may no longer reflect the current position.

Waiting until April. The tax year ends on 5 April. Planning done in March is reactive. Planning done in June for the following April is strategic.

Real-Life Scenarios

Earning £100,000. The priority is protecting the Personal Allowance. Even modest pension contributions or Gift Aid donations preserve the allowance and avoid the 60% effective rate band entirely.

Earning £125,000. The Personal Allowance is gone. The focus shifts to pension contributions to reduce adjusted net income, salary sacrifice to reduce NI exposure, and ISA maximisation for investment efficiency.

Earning £150,000. Pension tapering begins to apply, though annual allowance remains meaningful. Equity compensation planning becomes a priority. Family asset restructuring and inheritance tax basics come into view.

Earning £200,000+. Tapered annual allowance restricts pension contributions but does not eliminate them. VCTs and EIS become more relevant. Estate planning is no longer a future consideration.it is a current one.

Frequently Asked Questions

At what income level should I seriously start thinking about tax planning?

Earlier than most people do. The High Income Child Benefit Charge begins at £50,000, and by £100,000 the Personal Allowance taper creates an effective 60% tax rate that catches professionals completely off guard. If you are anywhere near these thresholds, the planning conversation should already be happening. Waiting until you are well above them means you have already overpaid for at least one tax year.

Is it worth making pension contributions just to protect my Personal Allowance?

Almost always yes. If your adjusted net income sits at £110,000, a pension contribution of £10,000 brings you back below £100,000 and fully restores the Personal Allowance. The effective tax saving is closer to 60% than the standard 40% higher rate relief when the restored allowance is factored in. Your pension grows, your tax bill falls, and the net cost of the contribution is significantly lower than the gross figure suggests.

My employer has offered me a large bonus. Should I take it or ask for it to be deferred?

It depends on where your adjusted net income currently sits. If the bonus pushes you across £100,000, you lose Personal Allowance on every £2 above that figure. Before deciding, check whether a pension contribution timed with the bonus payment would offset the threshold impact. The gross figure on the bonus letter is rarely what you actually keep without some planning around it first.

My partner earns significantly less than me. Does that create any tax planning opportunities?

Yes, and it is one of the most underused areas for high earners. Transferring income-producing assets to a lower-earning spouse shifts the tax liability to a lower rate. ISA allowances can be maximised across both partners. Pension contributions can be made for a non-working spouse. Viewed as a household rather than two individuals, the combined tax position often improves significantly.

How often should I review my tax planning arrangements?

At minimum once a year, and ideally at the start of the tax year rather than the end. Reviewing in April gives you the full year to act. Reviewing in March leaves almost no time. Income changes, bonuses, family circumstances, and threshold shifts all affect the optimal strategy. The professionals who consistently pay less tax than their peers review earlier and act on what they find.

Conclusion

The biggest financial challenge for most high earners is not generating income. It is keeping more of it efficiently and legally.

Threshold awareness, pension planning, family tax strategy, and investment efficiency are decisions that either get made deliberately or get made by default and the difference over a decade is significant.Lanop Business & Tax Advisors works with high earners across the UK to build proactive, year-round tax strategies managing adjusted net income, maximising pension opportunities, and ensuring no threshold is crossed without a plan already in place. If you are ready to keep more of what you earn, Lanop is ready to help.